Investing Money

There are times when you are very close to your financial goal and want to park your money for short term somewhere where it’s safe, it can easily be withdrawn and in the meantime get some reasonable returns. Here I am considering short term as less than 1 year investment horizon. There are three options to park your money for short term:

We would analyze these options one by one.

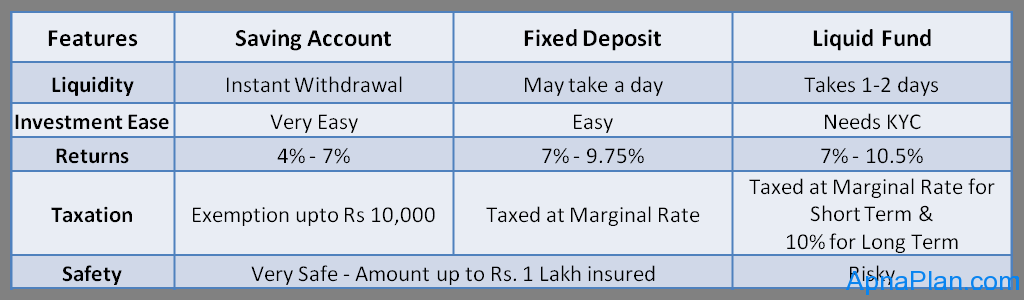

This is the default option. Whenever you withdraw your investments most of the time money directly comes to your savings account. So it’s the most convenient option. You can withdraw anytime you want.

But is Saving Bank Account the best place considering the returns front? It depends on the interest your bank is paying on your savings account and the amount of money involved.

The Saving Bank Account interest rate varies from 4% to 7%.

This is also easy option execution wise. If you have online banking, most of banks offer facility to do an online fixed deposit. So you can select the desired tenure and do an online FD.

Rate of Interest: 7% – 9.75% by different banks

For those who are not familiar with Liquid funds. Here is a brief – Liquid Funds come under the category of debt schemes offered by Mutual Funds. The basic objective of a liquid fund is to manage the short term cash surplus of investors and provide optimal returns with moderate levels of risk and high liquidity. Liquid Funds generate income primarily through interest accrual by investing in money market instruments like Commercial Papers, Certificate of Deposits, CBLO/ Repos and in short term debt instruments of corporate and NBFCs.

The investment process may not be as easy as bank FD as you would either need a demat account or invest online through respective mutual fund website or through some agent. Also you need to have KYC in place before investment. Also the liquidity is not as good as Savings account or FD which are instant. In case of liquid fund redemption it generally takes a day or two.

Returns: According to valueresearch the return in last 1 year varied from 7.05% to 10.45% with category average of 9.01%

Now that we have checked out returns and liquidity let’s look at the taxation part.

In case of Savings account interest upto Rs. 10,000 per year is exempted from income tax. After that the interest income is added to your income and taxed according to tax slab you fall in.

In case of fixed deposit the entire interest income is taxable. So total interest would be added to your income and taxed according to the tax slab.

Growth schemes of Liquid Funds are taxed as follows:

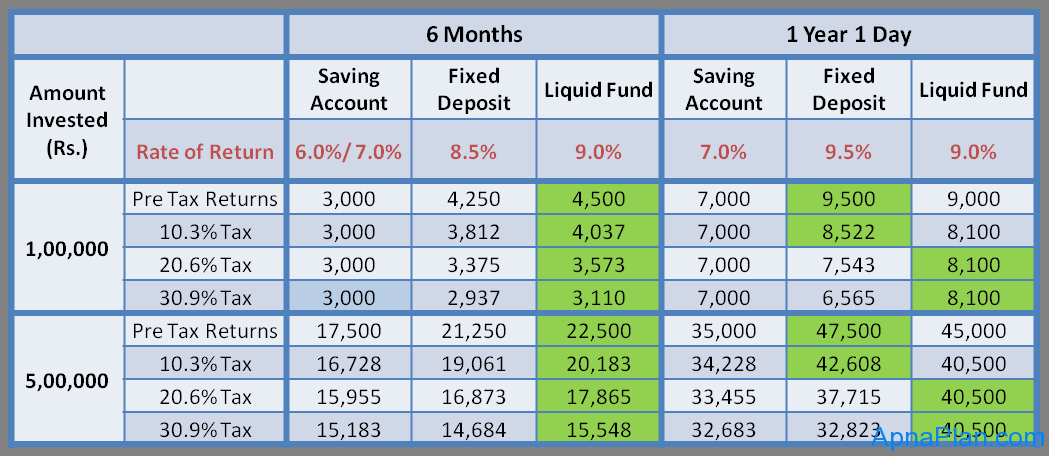

Now we know all the facts about returns and taxes let’s do some calculations about which is the best instrument to park your short term money.

For Calculation we make the following assumptions for returns:

| Short Term Options | Less Than 1 Year | 1 Year + |

| Savings Bank Account | 6.0%/7.0% | 6.0%/7.0% |

| Bank Fixed Deposit | 8.5% | 9.5% |

| Liquid Fund | 9.0% | 9.0% |

The table below shows the returns post tax when you invest Rs. 1 lakh and Rs. 5 Lakh for 6 months and 1 Year 1 day.

The cells with best returns are shaded in green.

The significant points to note are:

The decision to park short term money can be done based on your liquidity needs, amount to be parked, returns and taxes. So go ahead and do your calculations on finding the best short term investment for you.

Everyone hates paying taxes and always are on lookout for Options to Save Tax. However…

Are you worried and confused about Lien amount in SBI? Well you are not alone.…

Get details of latest Sovereign Gold Bond Price, Issue details, taxation and how to invest.…

Download the Excel based Income Tax Calculator India for FY 2020-21 (AY 2021-22). This compares…

Piramal Capital & Housing Finance, has come out with Piramal Capital & Housing Finance Ltd…

IIFL Home Loan, the Housing Finance company from IIFL Group has come out with IIFL…

{kind=link}

{kind=link}

View Comments

dear sir above article is quite good explain very good, but if the divident option and divident reinvest option is also considerede then article become nice try to add reinvest option,if FMP is also described then the article become more fruit ful

thanks