Employee Pension Scheme - EPS

If you have looked at your EPF (Employees’ Provident Fund) details you might have wondered about deduction of Rs. 541 per month from your company’s contribution to EPF.

Here is the explanation:

Here is an example of how EPF & EPS is calculated:

Suppose your basic salary Rs. 10,000 per month.

Since the basic salary is more than Rs. 6,500, only 8.33% of Rs. 6,500 (i.e. 541) is contributed to EPS.

First lets talk about the similarity between both – EPF & EPS. Both are Retirement Schemes compulsory for private company employees (employers with more than 50 employees) and are managed by EPFO (Employees’ Provident Fund Organisation). In case of EPF you get certain percentage interest on your deposits, which are decided by EPFO board every year. Whatever is the amount accumulated in this EPF account by the time you retire, you receive that as a lump sum.

In case of EPS, you get a monthly pension after you retire which is based on a formula. The good thing about this pension is, your wife/dependents continue to get this monthly pension even after your death subject to certain conditions.

The next logical question is how much pension would you get under EPS scheme? It’s based on a formula:

Monthly Pension = (Pensionable salary X Pensionable service) / 70

For e.g. you join a private sector company at the age of 25 and continue working there till retirement at the age of 60; with your basic salary always exceeding Rs 10,000 per month. Here is what your monthly pension amount would be:

Pensionable salary = Rs. 6,500 [even though your basic salary is Rs. 10,000 but there is an upper limit of Rs. 6,500]

Pensionable service = 60 – 25 = 35 Years

So, Monthly Pension Amount = (6500 x 35) / 70 = Rs. 3,250

You would receive this amount of Rs. 3,250 as your monthly pension for your life time and this would continue even after your death to your dependents.

This brings us to the next question –

Is EPFO justified in paying such a small pension for your contribution of Rs. 541 per month for 35 years?

Let’s do some number crunching and get the answers.

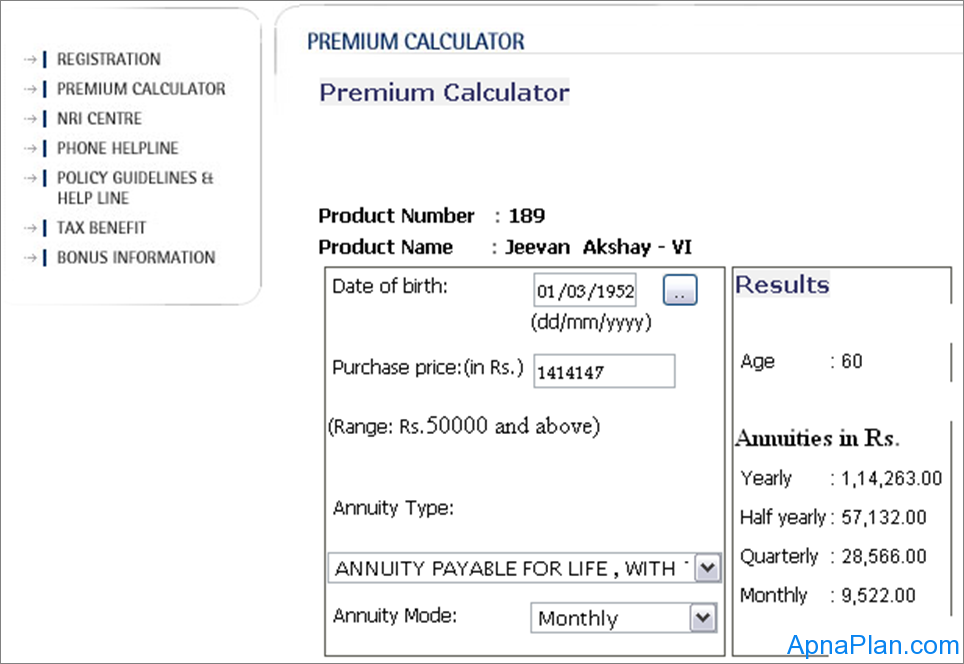

Had your contribution not gone compulsorily into EPS, it would have gone to your EPF (or VPF) account and paid to you in bulk at the time of retirement. Assuming a rate of interest of 8.5% for entire tenure of EPF, the monthly contribution of Rs. 541 for 35 years (or 420 months) would grow to Rs.14,14,147.

You can withdraw this amount and invest in annuity options available with Insurance companies for regular income. For simplicity I have chosen Jeevan Akshay VI Annuity plan from LIC (Life Insurance Corporation). Here you can invest lump sum amount and receive fixed amount every month. You can access the premium payment and benefit calculator on LIC website here.

I choose following options to keep the annuity plan similar to EPS benefits:

Once you enter these values and calculate – you would be surprised to know that you are eligible to receive Rs. 9,522 per month as annuity from LIC on your above investment.

This amount is almost 3 times the monthly pension paid by EPS!

Unfortunately there is nothing much we can do as the EPS scheme is compulsory by Government of India for all the members of EPF. But it’s good to be aware how some retirement plans by government are just an eye wash and your money wasted. Its time government & EPFO need to look at EPS & retirement plans and modify them to keep pace with current trends and returns.

Everyone hates paying taxes and always are on lookout for Options to Save Tax. However…

Are you worried and confused about Lien amount in SBI? Well you are not alone.…

Get details of latest Sovereign Gold Bond Price, Issue details, taxation and how to invest.…

Download the Excel based Income Tax Calculator India for FY 2020-21 (AY 2021-22). This compares…

Piramal Capital & Housing Finance, has come out with Piramal Capital & Housing Finance Ltd…

IIFL Home Loan, the Housing Finance company from IIFL Group has come out with IIFL…

{kind=link}

View Comments

Hi Sir, i found a blog finally which i am looking for. I still have the following queries . I want to talk only about EPS (not EPF or PF)

1) I am contributing to EPS from my 21st age. Lets say i contribute till my 60th age. Maimum pension amount i can avail is 7500. This amount i will receive till my death, after my death my wife will receive till her death, by that time my son/daughter will be more than 25 years of age. so i don't think they will get anything after we (parents died). so thats it, no amount will be given to our familes after my death and my wife death? Is my understanding correct.

2) If the above point is correct 1250 i am contributing monthly to EPS till my 60th age, which will be 1250x35yearsX12months= which will be 640000 nearly. With interest rate of PF/EPF this amount will be nearly 15 - 17Lakhs by my age of 60. Interest of this 15-17l is given as pension amount which is 7500 per month. Then what will happen to the original amount 15-17Lakhs, it is taken by government? or they will give this amount to my family on my death or my wife's death, whoever is later?

Thanks in advance.

Assuming a rate of interest of 8.5% for entire tenure of EPF, the monthly contribution of Rs. 541 for 35 years (or 420 months) would grow to Rs.14,14,147.

Can u tell me how this fig of 14 laks arraived. I got 1.2 lakhs only by calculation.

RMJoshi 9223550682

You are doing 541*420. My calculation is like recurring deposit of Rs 541 for 420 months @ 8.5% interest. This is what it means to be invested in EPF

if i have another pension scheme, will i be eligible for eps pension

Yes you would be eligible for EPS even if you have another pension.

Why , government can not allowed this accumulated amount in other annuity fund.

EPS is a black hole sucking subscribers money. Government should definitely try to improve on the same.... But as you nothing moves until we all unite and protest :(

EPF PENSION IS to just make industrial employees fool as they are making in the case of ESI. They are giving subsidies to villagers. for example if we are getting rice at Rs. 40 per kg, subsidised rice are available at rs. 4 per kg to villagers. on whose money this centre government is using. IS COUNTRY KO POLITICIANS NE NAHI MARA, IS COUNTRY KO INDUSTRIALISTS NE MARA HAI. TIME WILL COME WHEN THEY WILL BE RUINED OF THEIR WEALTHS, PENSION AUTHORITIES INCREASED MINIMUM PENSION TO 1000 RS. AND GOT THE VOTES FROM ILLETRATE PEOPLE. HARAMZADO JUST MENTION HOQ MUCH PENSION IS POSSIBLE FOR A PERSON WHO HAS WORKED FOR THIRTY THREE YEARS. YEH LOG SONE KE SIKKE DISTRIBUTE KARTE HAI ON THE OCCASION OF SILVER JUBILEE. ON WHOSE BEHEST. PF COMMISSIONERS INDUSTRIAL WORKERS KAA BLOOD KHA RAHE HAIN.

This article is indeed an eye-opener. The Government needs to clarify how it is utilizing our money in this fund, or is it using this as a cheap source of funds for continuing populist subsidies. It can easily generate 20,000 crores per annum (assuming 3 crore account holders), and at an interest rate of ~3% (whereas the market rate would be 8-9%)!

What would happen, if i quit company within 1 0r 2 year? Will my money will go to Govt pocket?

No if you stop working before completing 10 years of service, you have provision to withdraw your money.