With the recent notification of RBI (Reserve Bank of India) about limiting Non Banking Financial Companies (NBFC) to provide Gold Loan up to 60% of value of Gold Jewellary, it seems now rules of the game would be rewritten.

Now, banks might turn out to be better option for Gold Loan borrowers due to following reasons:

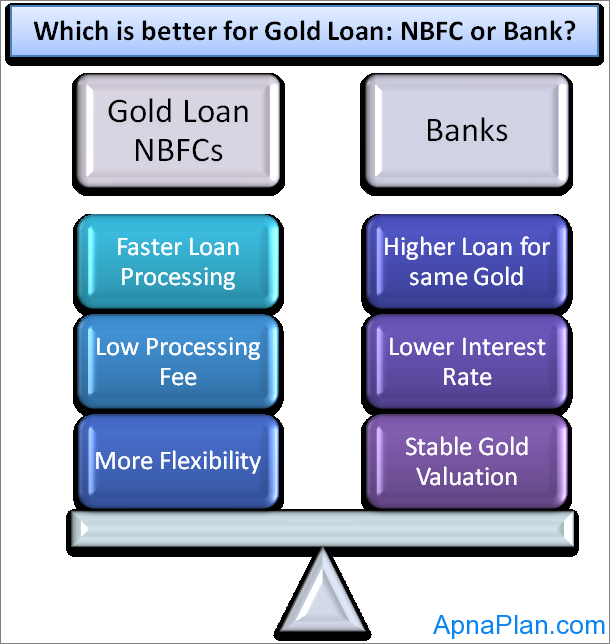

But NBFCs gain when it comes to loan processing time, processing fees and flexibility in duration of the loan.

For processing a gold loan request, banks charge around 1% of the loan value as processing charges and in some cases borrowers face an additional charge under stamp duty and assayer charges. Gold finance companies however have a very nominal processing charge and this again is a fixed amount and doesn’t vary with value of the loan. At Manappuram Finance for instance the processing fee is Rs 8 and from the second month of the loan the borrower is levied Rs 2 as renewal fee in addition to the interest.

Banks also take a relatively longer time to process a gold loan. This is generally because of the additional paper work and sometimes because of certain procedural delays and glitches at the back-end.

So now it’s you to decide what you want!

if you are looking for higher value of gold loan at lower interest rate bank might be a good option but if you want a more flexible approach with faster processing time NBFCs would be a better option.

Everyone hates paying taxes and always are on lookout for Options to Save Tax. However…

Are you worried and confused about Lien amount in SBI? Well you are not alone.…

Get details of latest Sovereign Gold Bond Price, Issue details, taxation and how to invest.…

Download the Excel based Income Tax Calculator India for FY 2020-21 (AY 2021-22). This compares…

Piramal Capital & Housing Finance, has come out with Piramal Capital & Housing Finance Ltd…

IIFL Home Loan, the Housing Finance company from IIFL Group has come out with IIFL…

{kind=link}