HDFC Click2Invest – Should You Invest?

HDFC Life encouraged with the response on its Online Term Plan Click2Protect has recently launched its online ULIP called Click2Invest. This is the first ULIP offered online exclusively after the IRDA new Regulations in 2010.

There are 8 options to choose from.

There are no policy allocation charges or Policy Administration charges, which reduce the initial corpus to be invested in most other ULIPs. This in turn impacts the returns.

There are only two charges – Fund Management Charge of 1.35% and Mortality Charges depending on your age.

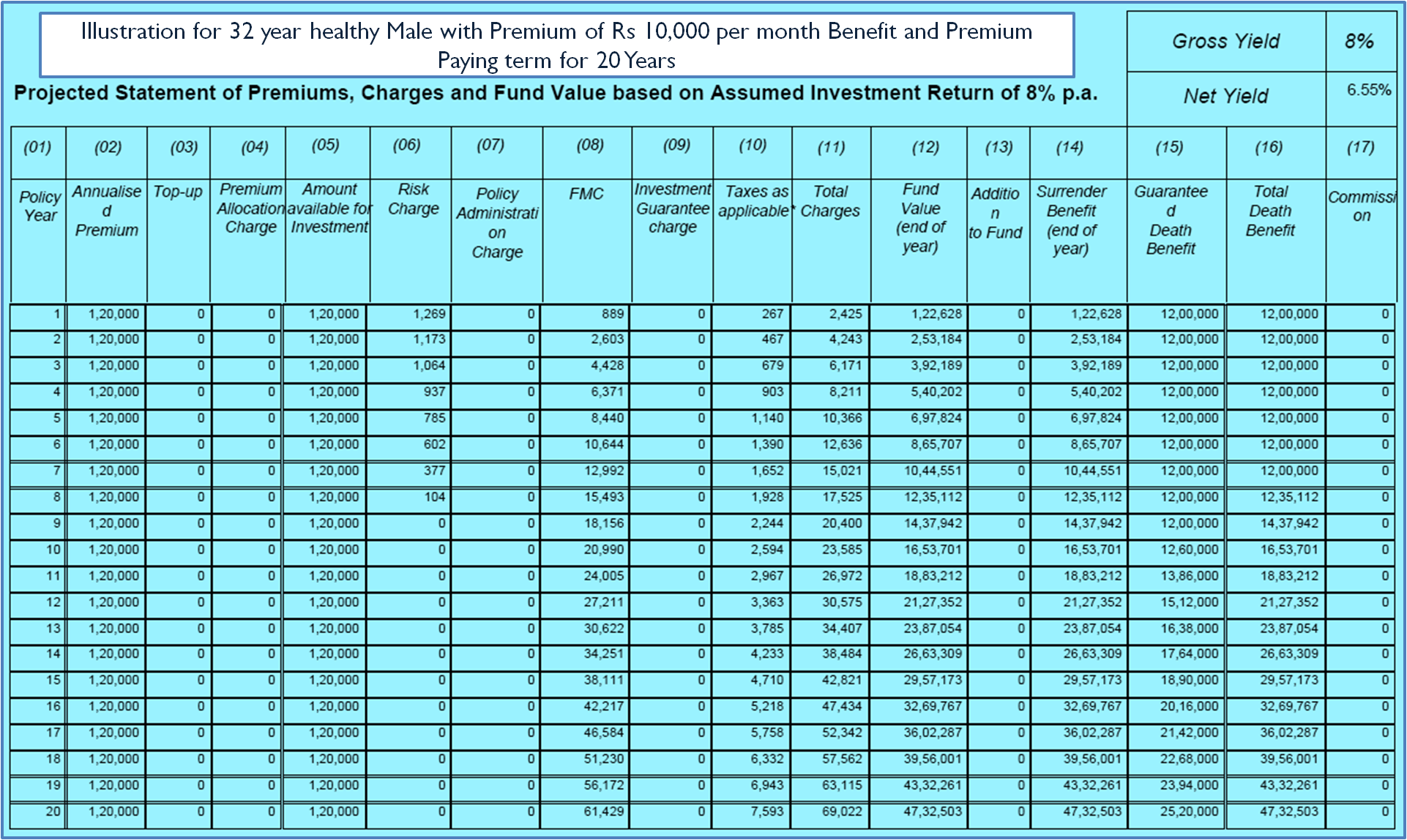

If you check the illustration below, you would find the net return is 6.55% on the gross return of 8%. This means only 1.45% is the net expense in the plan. Almost all (except Quantum Tax Saving Fund) Tax Saving equity mutual funds (ELSS) have expense ratio in excess of 1.5%, which means the HDFC ULIP is cheaper than most ELSS Funds.

As this is ULIP, it also carries death benefit which maximum of

So the nominee is assured of at least the sum assured part as soon as you enroll in the policy.

The sum received on maturity, surrender or maturity is tax free (Single Premium and People with more than 55 Years of age paying annual premium payment would not get tax benefit)

The ULIP allows 4 free switches between funds in a year. You can use this to shift your investment between debt and equity fund as per your asset allocation plan. You can also book profits from time to time by transferring money from equity to debt fund.

Also as the policy nears maturity it would be good idea to switch slowly to debt funds. You can do all this without any charges or tax implication.

As most ULIPs, HDFC click2invest too is complex product and so it would be very difficult even for a well educated person to understand all the clauses and if and buts of the plan.

Single Premium and People with age of 55 Years or more even with annual premium payment would not get tax benefit as their sum assured is less than 10 times the annual premium. Unfortunately HDFC Life has not made it clear in the policy document and I am sure this would lead to some misselling!

Even if you surrender the policy before completion of 5 years, the life insurance cover ceases and the fund is transferred to Discontinued Fund (offering just 4%) and can be withdrawn only after completion of 5 Years.

Though the total expense of the ULIP is less than most equity mutual funds but is higher than most liquid mutual funds. So if you want to choose the Income, Bond or Conservative Fund you would do better investing in Debt oriented Mutual Funds

Higher your age at the time of taking the policy lower would be your return. This is mainly because for higher age the mortality charges go up and dents the returns.

You need to pay the premium every year at least for 5 Years. If you don’t your life insurance cover ceases to exist and the fund is transferred to Discontinued Fund offering just 4%.

Financial Advisors generally advised to keep insurance and investment separate and I too agree with them. Nevertheless HDFC Click2Invest suits those who

HDFC Click2Invest ULIP is being offered only online and hence has enabled HDFC Life to cut a lot of expenses. It’s truly a low cost plan especially if you compare with ELSS (Tax Saving Mutual Funds). But as with most ULIPs, it’s a complex product to understand. Therefore most financial advisors advise to keep insurance and investment separate.

Also note that Single Premium and People with age of 55 Years or more even with annual premium payment would not get tax benefit. So anyone with age more than 55 Years should totally avoid this ULIP.

You might want to invest if you are looking for longer maturities to benefit from low cost and want to use the switching benefit for asset allocation. Personally I would keep away due to its complexity and its non-flexible nature.

Everyone hates paying taxes and always are on lookout for Options to Save Tax. However…

Are you worried and confused about Lien amount in SBI? Well you are not alone.…

Get details of latest Sovereign Gold Bond Price, Issue details, taxation and how to invest.…

Download the Excel based Income Tax Calculator India for FY 2020-21 (AY 2021-22). This compares…

Piramal Capital & Housing Finance, has come out with Piramal Capital & Housing Finance Ltd…

IIFL Home Loan, the Housing Finance company from IIFL Group has come out with IIFL…

{kind=link}

View Comments

Hi my age is 25 I want to investment in click2 plan every month 2500 to 3000k also want to save tax..so please advise that is good for me or I need to buy any other plan if any other which one I need to buy...

Hello, thank you for wonderfull blog. It really helped me a lot. I am looking to invest in SIP in ELSS. I don't know much about it. My age is 25. Can you provide me link to give all of the information? also can you please name a best policy just for investment purpose. Thank you looking forward to hear from you.

Best ELSS (Tax Saving Mutual Fund) to Invest in 2017

Hello sir

Plz can you suggest me how is HDFC life click to invest plan opportunity fund and income fund 60& 40 ratio .I want to invest 5000 P/m for 15 yrs.

Plz advise me I will go for this fund or any other

Thanks

I am not sure why you want to invest in ULIP. My recommendation invest in mutual fund and take term life insurance

Hi.. I am looking for a long term investment option for my 1year old. I would want your views on the sec 10.10D benefit. Do u think beyond a premium value.. The tax benefit exceeds the oncremental/additional cost of insurance when compared to pure term plans

You should not opt for ULIP if you are investing for your children. A few months back I had done post on child specific mutual fund plans and concluded that a sufficient term insurance and mix of equity funds are good investment for children long term goals. If you are looking for extreme safety I would recommend PPF rather than ULIP. Also if you are worried about tax benefits you must go through the tax planning ebook.

I am looking for a long term 15-20 yrs with a low invesment of 15-20k per year. Only for investment purpose and not for insurange . will this plan be suitable

I would suggest Equity based mutual funds as it offers flexibility. You can easily change your SIP amount or withdraw without any tax hassles. ULIP though have become more cost effective but still is complex product.

Hi Amit,

I am working in an IT firm from past 2 years. Age – 25.

Suppose I have Rs.5000 a month which I can invest as an investment/insurance. I don’t have much knowledge about these investment/insurance stuffs.

In a layman language , I want to invest(which should include tax savings) my Rs.5000(or more if you say) a month to somewhere where I could get good return after maturity period(can be 10/10+ years) as well as I want to have a life insurance cover so that in case of any mishappening my dependents would get something.

As you have already mentioned above that one should not combine investment and insurance , can you please suggest me how I should divide my Rs.5000 to achieve above.

One more thing I had invested in Click2Invest(Quaterly 15k – paid premium two times till now i.e. a total of 30k). I am thinking of discontinuing it coz almost everywhere online I am seeing that click2invest is not good. As per the TnC of Click2Invest I know that I wont be getting my 30k back before 5 years. I know I should have consulted before buying it.

HDFC life ppl have automatically invested 100% into Opportunity Fund – I know I can change it but I am not sure what is it all about so I left it as it is.

Its good to see someone at 25 reading about investment and insurance. As you say you want to invest Rs 5,000 per month and also want insurance and tax saving. You would be surprised to know that term life insurance is pretty cheap. A cover of Rs 1 crore for non smoking 25 year old is available online for annual premium of Rs 7,000. As you are looking for tax saving + long term wealth creation, you should do SIP in ELSS (Tax saving mutual fund).

The good thing about Click2Invest is its low cost but ULIPs are generally not advisable investment as the structure is complex and there is lack of transparency. Confirm with HDFC Life Insurance what happens in case you stop paying premium now.

hello sir,

i want to invest 2000 per month for a period of 20 years in HDFC click to invest ,what return i am looking for as different representatives giving me different no.

also should i invest in this policy or kindly suggest any other policy if there in your mind.

i want to go forward for long term investment.

There is no one who can tell you accurately how much you will get at maturity. Everyone assumes a rate of return (4% & 8% is approved by IRDA) and thus the returns vary depending on the rate you choose.

I would still advise you to opt for equity based mutual funds for investment part and take Term plan for life insurance.

Dear Sir,

I buy HDFC lick to invest in balance fund, I pad 1000 monthly for last eight months and I invest it for total 5+5 years.

My sum assured is 120000 Rs after 10 years should I believe on it..?? Because my fund value is always come less than what I pad to HDFC.

Please suggest me what can I do...!!

Balanced fund in the above ULIP can have 40% to 80% exposure to equity, so your investment would mirror the performance of stock markets; which is not great at the moment. Having said that ULIPs are long term products and the expenses are high in the initial years on account of higher deduction towards mortality charges as you can see in the illustration in the post.

As I would suggest to invest in Mutual Fund + Term Insurance rather than ULIPs as ULIPs returns might be poor than the same category mutual funds.

Hi I am willing to invest in this plan. Is it good idea to invest in this plan? will it provide good returns. I need to invest for 10 years with tax benefit. I am 25 yr male . I did not have any life cover till date. So is it worth to take this plan or should I go for some other.

As I said in the post I am not comfortable with ULIPs due to their complex nature and inflexibility. So I would advise to do Term plan online an choose good mutual funds for investment.